Electric vehicles (EVs) are powered by electricity rather than internal combustion engines that run on fossil fuels. Every EV has a battery, and every battery relies on EV battery material. Indonesia is a primary source of many of these, including lithium, nickel, cobalt, copper, and graphite. However, the abundance of these resources does not answer the more complex question of how ready Indonesia’s EV ecosystem is in the eyes of investors.

An earlier INTRA Institute’s study, Business and Investment in Indonesia’s Critical Minerals as Primary Sources to Electric Vehicle Production, mapped the country’s EV value chain and revealed a strong presence of foreign direct investment (FDI), particularly in higher value-added segments. While the findings highlighted Indonesia’s strategic position in global supply chains, the results also pointed to a more fundamental question: what shapes investor confidence and appetite to invest?

To explore this, INTRA Institute, the knowledge generator unit of Angin Dampak Jaya, publishes A Preliminary Look into Investor Confidence and ESG in Indonesia’s Electric Vehicle (EV) Sector (2026), a research report based on in-depth interviews with five institutional investors and stewardship consultants with total AUM ranging from IDR 12.69 trillion to EUR 214.1 billion.

Context: The Scale of a Transition Already Underway

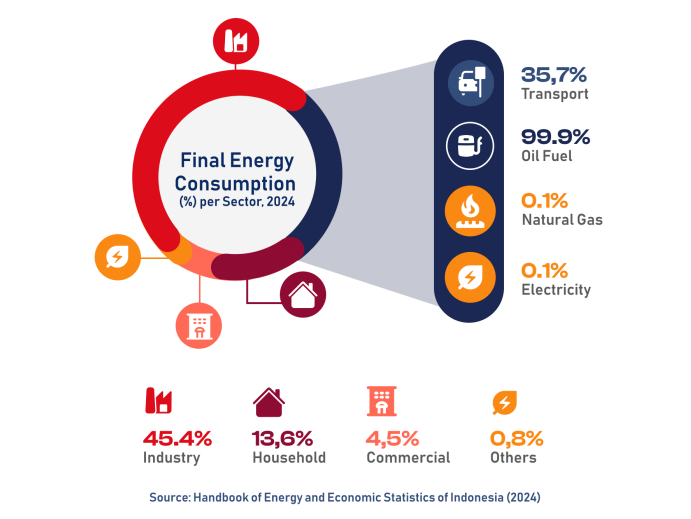

The shift to electric vehicles is happening rapidly. Global EV sales increased from 0.2 million units in 2014 to 10.8 million in 2024. As transportation accounts for 21% of global carbon emissions, passenger vehicles are a significant contributor to this figure. In Indonesia, however, the situation is different. Transportation accounts for 35.7% of the country’s total energy consumption, 99.9% of which still relies on oil. Electricity powers just 0.1%.

The Indonesian government has responded with a concrete policy framework. Minister of Industry Regulation 28/2023 establishes the 2020-2030 EV development roadmap, which covers market, industry, and technology development strategies. In addition, the Minister of Finance Regulation 69/2024 grants tax holidays for industries supporting the EV value chain. This includes the nickel processing and EV manufacturing. The adoption targets set are ambitious, with projections showing a steep growth trajectory through 2034.

The Missing Link in Indonesia’s EV Ambitions

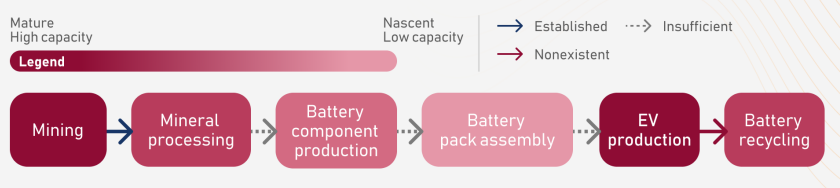

INTRA Institute’s report maps Indonesia’s EV value chain from the ground up. It also uncovers a disparity that directly determines where capital flows and where it stops.

At the upstream end, things look solid. Mining is mature, well-regulated, and operating at high capacity. Mineral processing has been growing steadily since Indonesia enforced its raw ore export ban in 2014. Both segments share something that investors find hard to resist: long operational track records, stable growth, and the kind of transparency that comes from being publicly listed.

Moving downstream, the picture changes significantly. Battery component production is still in its early stages, with only a few companies operating in this field. The battery pack assembly industry is heavily dependent on imports. In 2024, EV production hit approximately 25,861 units. This figure is bolstered by import duty policies that slashed the cost of assembled EV parts.

Battery recycling is practically nonexistent at the far end of the chain. There’s just one active facility, and it’s operated by a company that’s not making enough electric vehicles to generate enough material for commercial recycling operations.

A pattern of ownership runs through all of this. Domestic players are strong in mining, but as the Indonesia EV value chain moves further downstream, the domestic share shrinks. Foreign investment in Indonesia’s EV industry, particularly from China, is becoming increasingly dominant. This indicates that Indonesia has yet to translate its upstream advantage into local industrial capacity where it matters most.

Capital Flows Where Certainty Exists

According to the INTRA Institute Report, mining and mineral processing are still the main drivers of investment in the Indonesian EV supply chain. This is because they have strong profitability records and are directly linked to global demand. The EV manufacturing segment is viewed differently. New companies have to deal with a lot of challenges at the same time, like building production scale, securing the supply chain, and meeting changing regulatory standards. On top of that, they have to deal with an uncertain return on investment (ROI) timeline.

Structural barriers make this even worse. Out of the 17 companies on the IDX involved in the EV value chain, only 7 focus on EV manufacturing as their main business, which makes it harder for public market investors to get in. Most EV players stay private because the IPO requirements are really strict, and they like to raise money through private investors or joint ventures. The result is a disconnect between the ambitions of EV policy, public capital readiness, and investment opportunities that are accessible to the public. As long as there aren’t more investment options in the EV sector, ESG funds won’t automatically grow the EV ecosystem, and investors will stay cautious about EV Indonesia.

Who Shapes Where EV Investment Goes in Indonesia

The investment in Indonesia’s EV sector doesn’t just come from one type of investor. Instead, they show how important people interact. There are conservative asset owners, like pension funds and sovereign wealth funds that focus on preserving capital in the long term. Then there are asset managers who allocate that capital toward liquid and transparent public assets. Also, there are multilateral development banks that tie loan disbursements to strict ESG metrics. ESG consultants and third-party auditors provide technical validation for risks that can’t be assessed in-house. In addition, civil society organizations and media serve as watchdogs against greenwashing and social or environmental conflicts.

The interaction between these actors ultimately determines where capital flows. On one hand, the demand for sustainable investment products keeps growing. But there aren’t many pure-play EV companies on the Indonesia Stock Exchange, so capital stays focused on the upstream sectors. On the other hand, ESG oversight operates through multiple layers, combining corporate disclosures with third-party data.

At the same time, the pressure to move away from coal-based supply chains is growing. Standards like IRMA and RMI are becoming basic requirements for financing, instead of extra benefits. From a policy perspective, investors aren’t just looking for financial incentives. They also want long-term regulatory certainty to protect their investments from sudden policy changes.

Amid these dynamics, asset managers are increasingly positioning ESG as a competitive advantage to attract asset owners:

- Hidden risk assessment: Finding risks that can’t be seen in regular financial reports.

- Access to green investments: Serving as a doorway to eco-friendly financing for investors worldwide.

- Alignment with global mandates: Adjusting strategies to meet the sustainability criteria of large asset owners.

- Reputational risk mitigation: Combining third-party data and media monitoring to protect portfolio legitimacy and long-term returns.

- Proprietary standards: Developing internal frameworks that go beyond commonly used ESG screening approaches.

- Data transparency: providing measurable ESG reporting as a way to stand out in a market where there’s still limited competition.

ESG in the EV Supply Chain: A Demand Not Yet Met

ESG is no longer just about reputation. As of the third quarter of 2025, global sustainable fund assets had grown to more than US$3.7 trillion. This number is a significant rise from US$2.5 trillion in the last quarter of 2022. Big-time investors like Institutional Investor A have already put 20-25% of their assets into ESG products. In the future, they’re aiming for 30 to 35 percent.

But ESG implementation in Indonesia’s EV supply chain still has a long way to go. The INTRA Institute report talks about four main risks for EV investors in Indonesia:

- Unstable Policy Environment

Policy uncertainty and sustainability risks, compounded by political and global dynamics, are raising concerns over Indonesia’s ability to scale its EV and ESG agenda, weakening long-term investor confidence in Indonesia’s EV sector. - ESG Treated as Compliance Rather Than Risk Management

ESG is still treated as a compliance obligation and CSR program rather than a risk management framework. ESG risks such as human rights violations, supply chain disruptions, and environmental damage are estimated to cost the global economy up to US$58 trillion. - Limited Independent Verification Mechanisms

Investors increasingly require certification from bodies such as IRMA and RMI, key pillars of ESG regulations in Indonesia’s mining sector, for companies operating in mining and mineral processing. - Declining Global FDI

The decline in global FDI since 2022, driven by geopolitical instability, adds another layer of uncertainty for investors evaluating long-term commitments in Indonesia.

What Investors Actually Look For

Investor confidence isn’t based on just one thing. INTRA Institute’s report shows that investors look at a few things when they’re deciding how to invest. They check out how well companies are disclosing information, how reliable the external verification is, and how ESG is handled as a strategic issue instead of just an administrative one. In Indonesia, where the EV ecosystem is still taking shape and regulations are always changing, these three things become the deciding factors for whether a company or ecosystem is worth investing in long-term.

- Verified transparency.

Investors are more likely to trust companies that are honest about the ESG gaps in their business and have a plan to improve, rather than companies that make exaggerated claims that can’t be checked. The implementation of PSPK 1 and PSPK 2 on climate-related disclosures in 2027 is said to be a potential catalyst for more systematic ESG regulations in Indonesia’s mining sector. - Sector-specific certification.

For upstream segments, standards such as IRMA, RMI, and ICMM are increasingly required as due diligence tools, rather than being optional add-ons. These certifications provide stronger assurance than self-reported disclosures because they involve independent audits of environmental, social, and governance aspects that are unique to extractive industries. - ESG at the board level.

Companies that integrate ESG into business strategy and risk management with active board-level involvement are seen as offering stronger protection against investment volatility. Risks for EV investors in Indonesia, such as social conflict in mining areas, environmental regulatory shifts, or supply chain disruptions, require strategic responses, not just annual CSR reports.

The findings make one thing clear. ESG is no longer peripheral to investment decisions in Indonesia’s EV sector. Investors now consider ESG performance to be a key risk factor, not just a way to manage reputation. Loan payments from international banks are linked to how well they perform on ESG metrics. Investors are worried about their reputation if they’re tied to coal operations, so they’re pushing for cleaner energy transitions from local partners. And when the media reports on or civil society finds violations of labor or environmental laws, divestment follows. Investors are also checking claims for themselves, using third-party data from sources like RepRisk and Sustainalytics instead of just relying on what companies tell them. ESG is now a deciding factor, not just a footnote.

More About Critical Minerals and Indonesia’s EV Investment Landscape

To explore the full analysis on investor profiles, ESG implementation in Indonesia’s EV supply chain, case studies, and Indonesia’s EV policy outlook, download and read the full INTRA Institute report by Angin Dampak Jaya, A Preliminary Look into Investor Confidence and ESG in Indonesia’s Electric Vehicle (EV) Sector, and see where Indonesia’s EV supply chain investment story is truly headed.

This was beautiful Admin. Thank you for your reflections.