Critical minerals are mining commodities that hold strategic value for both the economy and national security, yet are highly vulnerable to supply disruptions due to a lack of adequate substitutes. Their definition varies across countries, depending on economic importance, use in strategic industries, market dynamics, and contribution to national resilience. In Indonesia, the Ministry of Energy and Mineral Resources has classified 47 minerals as critical, including nickel, copper, bauxite, and tin.

These minerals are not merely export commodities. They are the EV battery raw materials that will determine how far Indonesia can position itself in the global energy transition, particularly through the electric vehicle value chain. The question is no longer whether Indonesia possesses these resources, but to what extent they are being utilized domestically.

The report Business and Investment in Indonesia’s Critical Minerals as Primary Sources to Electric Vehicle Production, published by INTRA Institute, the subthink-tank unit of Angin Dampak Jaya (YADJ/ANGIN Advisory), addresses this question. Using a corporate stakeholder mapping approach and a desktop review of corporate annual reports, industry association data, and publications from research institutions and media, the report maps ownership structures and investment dynamics across each segment of Indonesia’s EV value chain.

The Pressure to Move Faster

The transportation sector accounts for 35.7% of Indonesia’s final energy consumption, with 99.9% still reliant on oil-based fuels. Electricity, meanwhile, contributes only 0.1%. This represents a direct constraint on Indonesia’s target of achieving net-zero emissions by 2060 and presents a challenge to the country’s broader critical minerals energy transition strategy.

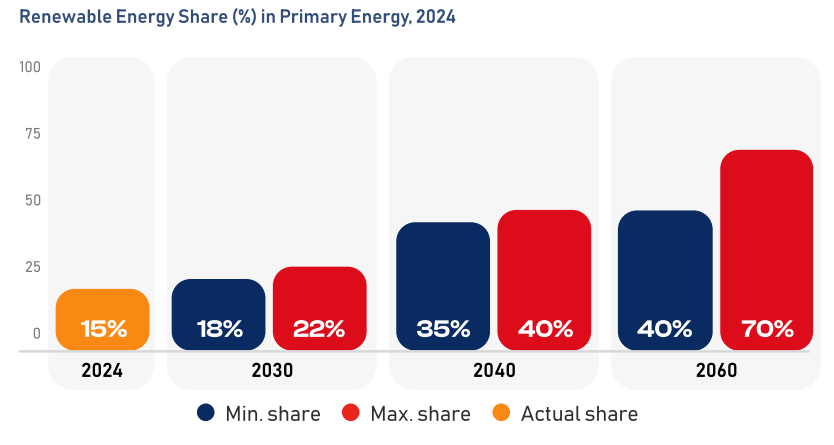

To reach this target, the National Energy Policy (KEN) 2025 mandates a progressive increase in the share of renewable energy. From the current 15%, the target is set at 18–22% by 2030, 35–40% by 2040, and 70% by 2060. The electrification of transport is one of the most tangible pathways toward achieving these goals.

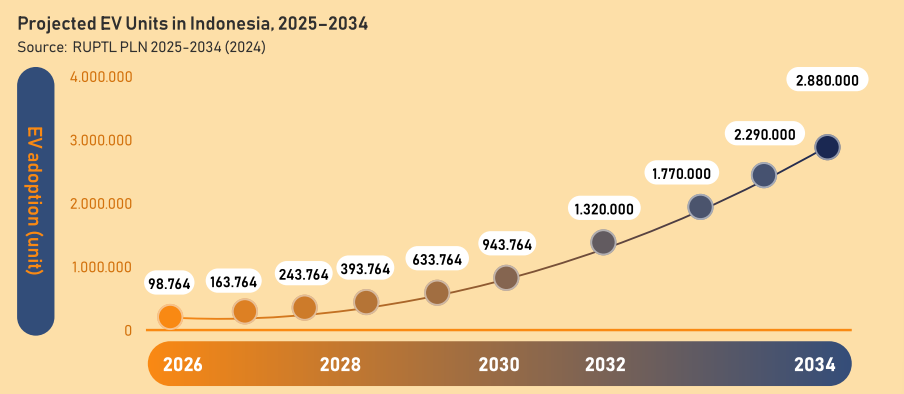

The government has set an ambitious EV adoption target through Minister of Industry Regulation No. 28/2023. From 98,764 units in 2026, the figure is projected to surge to 2,880,000 units by 2034. Achieving this scale requires a fully functioning value chain, from upstream mining to vehicles on the road.

Strong Upstream, Fragile Downstream

Indonesia accounted for 59% of global nickel production in 2024, with output reaching 173,635,642 metric tons. The national mining industry has attracted USD 47.36 billion in foreign investment and generated USD 34.1 billion in nickel export value. This is a solid foundation.

But that foundation is not yet fully connected to the downstream sectors. The INTRA Institute report maps six segments of the EV supply chain minerals landscape and their current conditions:

- Mining: Mature, with established regulations and relatively strong domestic dominance.

- Mineral processing: Expanded following the 2014 ore export ban, but capacity still falls short of demand.

- Battery component production: Still at an early stage, with only a few players such as PT HLI Green Power and Intercallin.

- Battery pack assembly: Heavily reliant on imports.

- EV production: around 25,861 units in 2024, partly supported by import duty policies on components.

- Battery recycling: Almost non-existent; only one active facility, while EV adoption stands at just 0.2%.

Ownership Map: Who Controls What

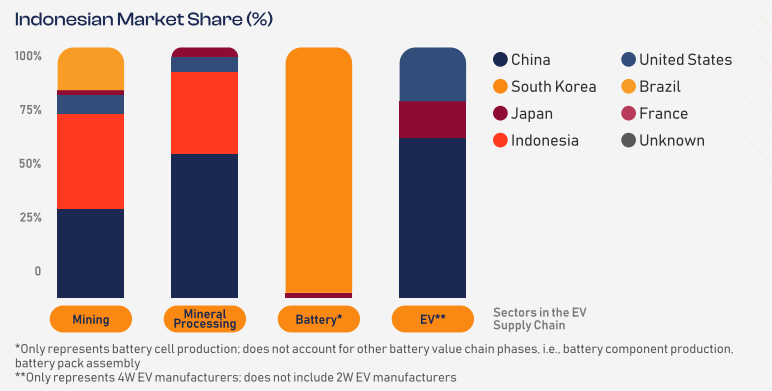

The report identifies 10 holding companies from five countries in mining, 17 in mineral processing, three in battery production, and six in EV manufacturing. The pattern is clear.

In mining, Indonesia still leads with a 48.55% share, supported by MIND ID and PT Trimegah Bangun Persada. However, this is the only segment where domestic dominance remains intact.

In critical mineral processing, China has taken the lead with 54.92%, while Indonesia follows at 38.36%. Names such as Tsingshan Holding Group, Lygend Resources, and Zhejiang Huayou Cobalt appear repeatedly, often through partnerships with domestic players. In battery production, South Korea dominates through joint ventures such as PT HLI Green Power. Meanwhile, in EV manufacturing, China controls 83.55% of the market share.

This means that the higher the value added, the smaller Indonesia’s share becomes within the value chain. Critical mineral downstreaming remains the weakest link in Indonesia’s EV value chain.

Why Non-Chinese Investors Are Reluctant to Enter

China is able to take positions in high-risk segments because it is backed by strong domestic economic capacity and supportive foreign policy. Investors from other countries do not have the same cushion.

The report highlights several factors that consistently shape investment decisions. Regulatory uncertainty is one issue, with tax schemes, export quotas and permitting rules often shifting mid-feasibility, which stretches timelines and strains business cases. Then there’s the broader slowdown in foreign direct investment (FDI) that UNCTAD has tracked since 2022, with LG Energy Solution’s exit from Project Titan being the most visible local example. Responsible sourcing also remains a genuine sticking point, particularly given the environmental and labour concerns associated with nickel operations in Morowali and Halmahera.

The full report covers in depth what is driving each of these issues and how they interact.

Gaps in Critical Mineral Value Chain That Remain Unaddressed

Beyond foreign investment, there are structural issues that explain why Indonesia’s domestic value chain stops short.

Intermediate products are one part of this process. Companies such as Huayou reportedly ship precursor materials to China for further processing before they reach end buyers such as Tesla, Volkswagen and Ford. Even when the raw materials come from Indonesia, value addition happens elsewhere.

The policy hasn’t caught up either. There is no distinction between NMC-powered EVs, which draw on domestic nickel, lithium and cobalt, and LFP-powered EVs that rely on imported materials. Meanwhile, the 40% TKDN threshold only applies to government and SOE procurement, leaving the private sector largely outside its reach.

The full report covers how these gaps translate into concrete investment and policy implications.

For businesses, investors, and policymakers operating in this sector, the report underscores several key points:

- Indonesia holds a clear comparative advantage in nickel and cobalt mining, with significant global market share and a long track record of investment.

- Critical mineral processing for EVs has expanded, but remains dominated by foreign investment, particularly from China, and is not yet optimally linked to downstream value chains.

- The largest gaps lie in the midstream and downstream segments, where domestic capacity remains limited and policy instruments have yet to fully support local resource absorption.

- Responsible sourcing concerns and regulatory uncertainty continue to pose real barriers to non-Chinese investment in higher value-added segments.

In other words, Indonesia’s critical minerals are not merely geological assets. They are a key variable in the global energy transition, one that is still waiting to be fully optimized domestically.

Learn More About Indonesia’s EV Value Chain Investment Landscape

For a comprehensive analysis, including shareholding mapping, investment case studies, and policy recommendations, download and read the full INTRA Institute report by Angin Dampak Jaya (YADJ/ANGIN Advisory), titled Business and Investment in Indonesia’s Critical Minerals as Primary Sources to Electric Vehicle Production.